Holistic Advisory

Comprehensive advice tailored to your unique needs, ensuring every aspect of your financial life is optimized.

You & Your Goals

Your aspirations are our priority, and we craft personalized strategies to help you achieve them.

Constant Support

Always by your side, we offer a steady hand, ensuring you have the support you need when you need it

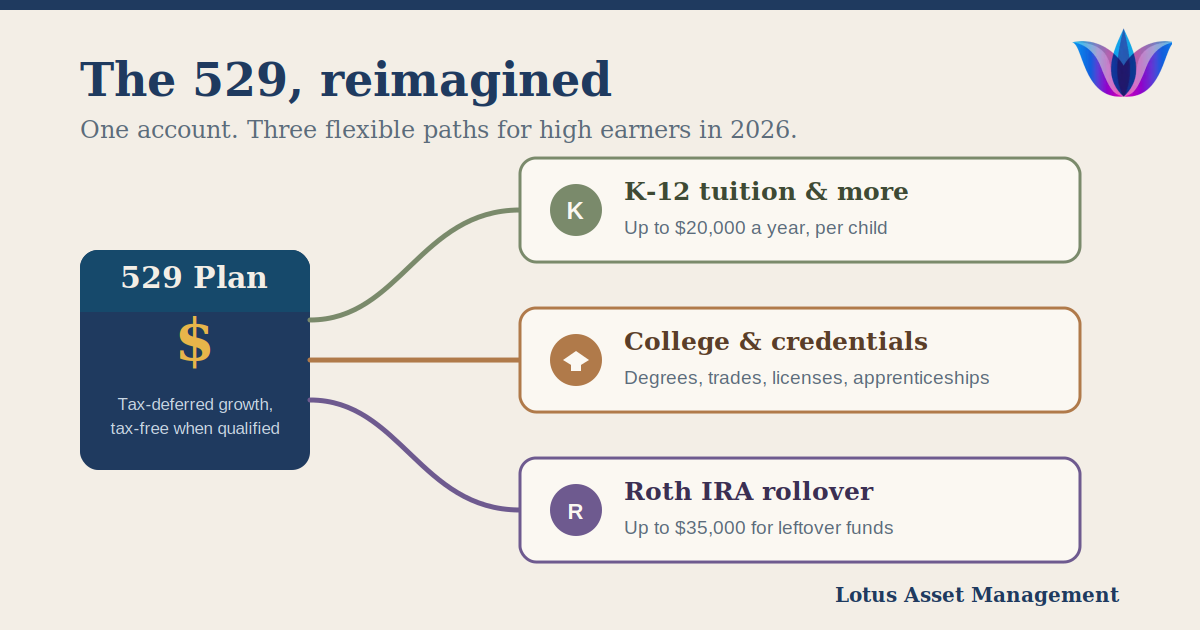

The 529 Plan Got a Major Upgrade. Here's How High Earners Should Use It in 2026

Read more

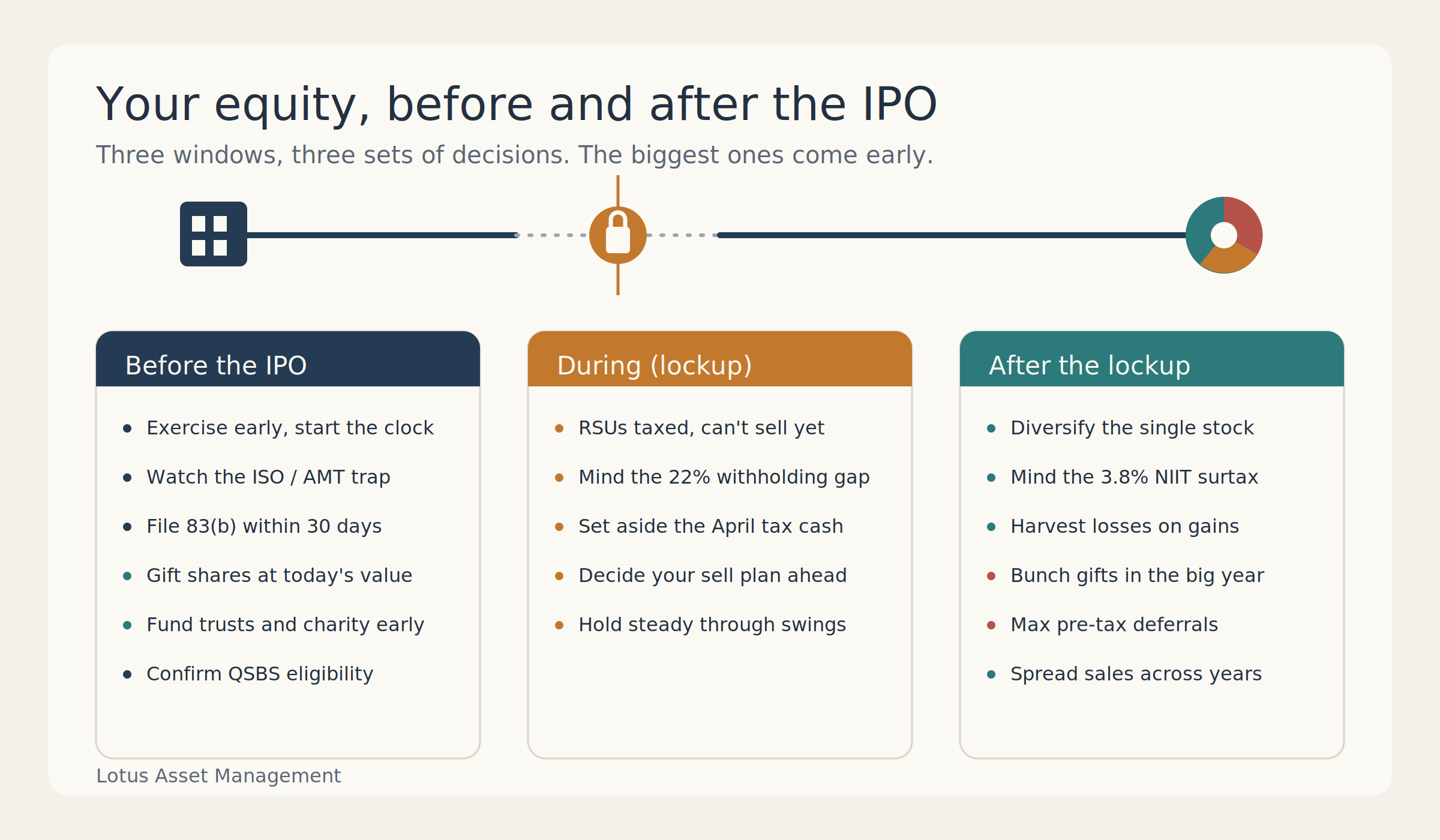

Your Company Might IPO Soon. Here's What to Do With Your Equity Before, During, and After

Read more

When One Stock Becomes Most of Your Net Worth, What Should You Actually Do?

Read more

How Does the Mega Backdoor Roth Work, and Who Actually Qualifies?

Read more

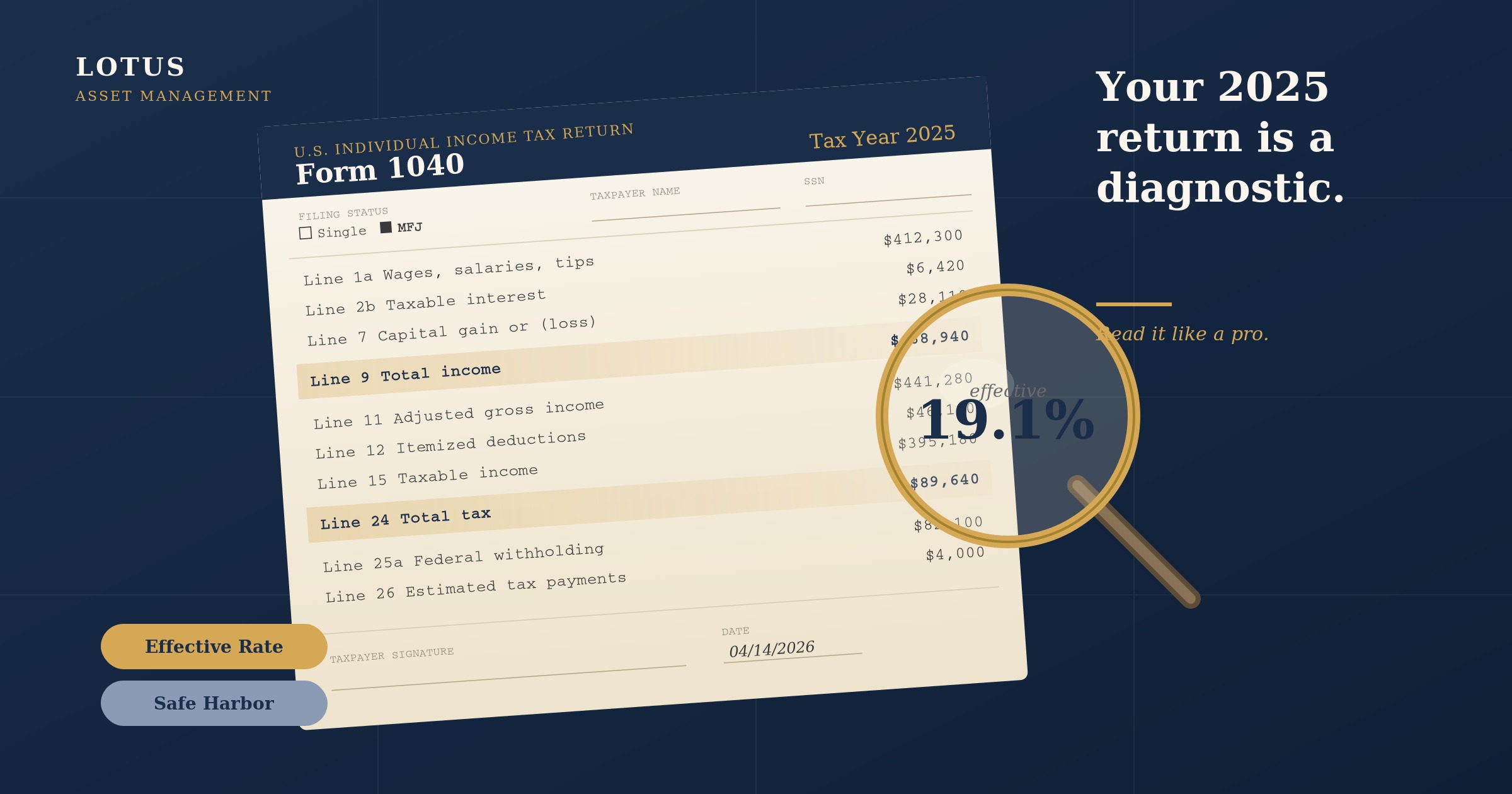

What your 2025 Tax Return is Actually Telling You (continued)

Read more

What Your 2025 Tax Return Is Actually Telling You

Read more

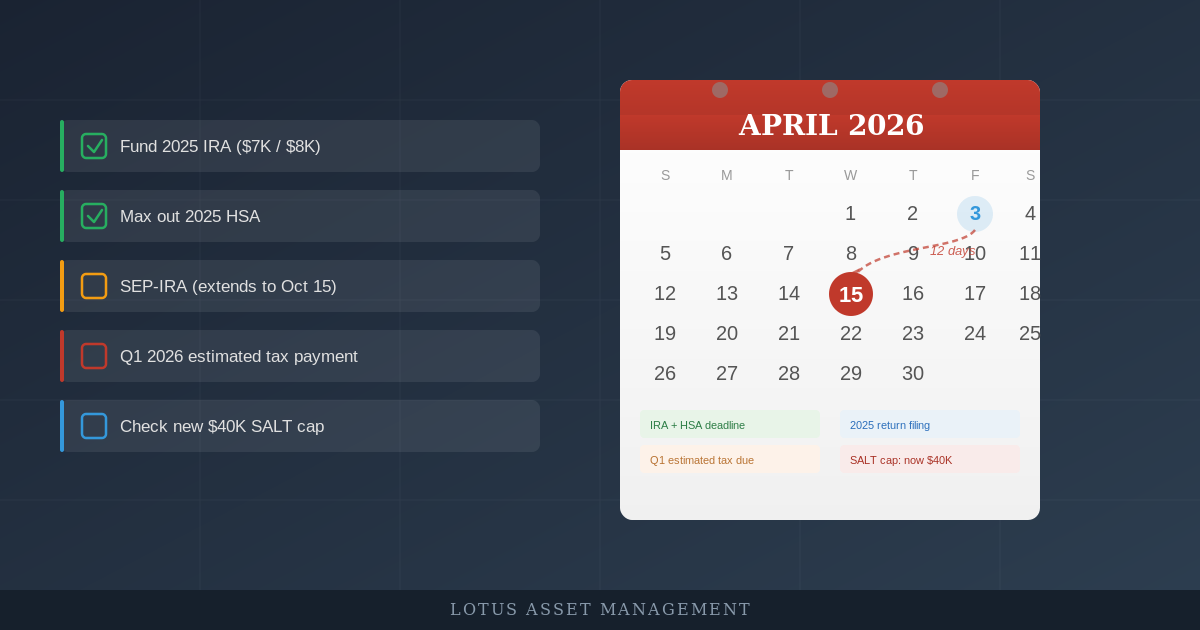

Which Tax Moves Expire on April 15 – Even If You File an Extension?

Read more

Market Volatility in 2026: What High Earners Should Actually Do With Their Portfolio Right Now

Read more

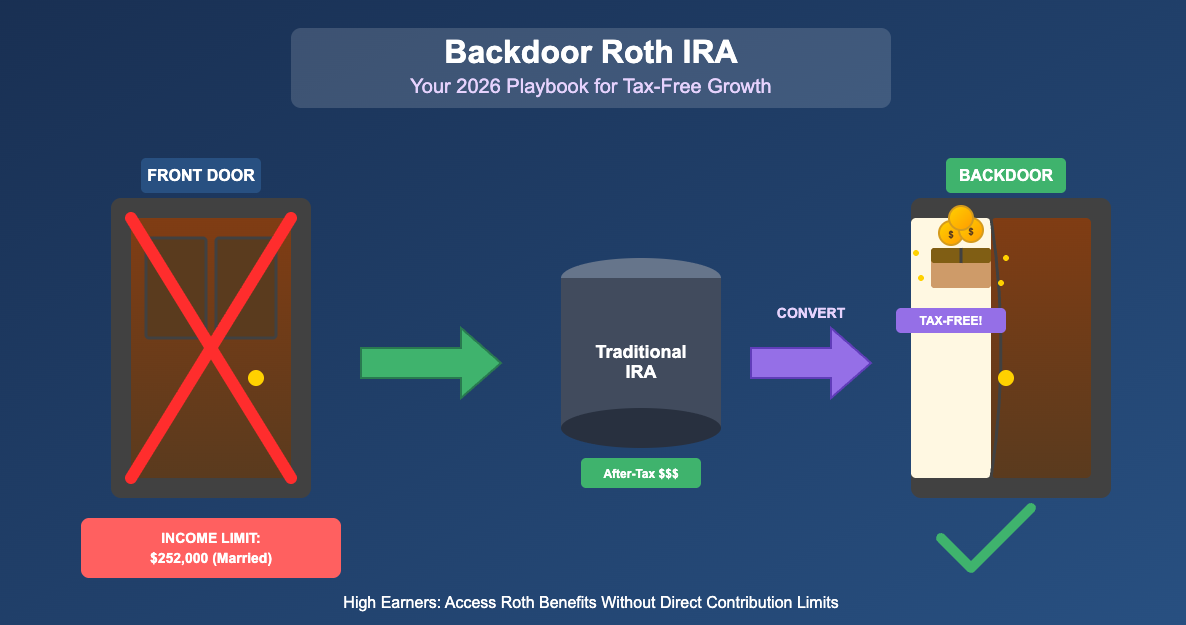

Backdoor Roth IRA Strategy for 2026: How High Earners Can Still Access Tax-Free Growth

Read more

Tax Season 2026: Why Filing Smart Beats Filing Fast

Read more

2026 Tax Planning for High Earners: How to Turn Updated Rules Into an Advantage

Read more

Why You Should Recalibrate your Retirement Strategy BEFORE the New Year

Read more

How to Maximize Year-End Tax Moves Before December 31st

Read more

When “Fixed” Isn’t the Default: Navigating ARMs for Young High-Earners

Read more

Open Enrollment - Dos and Don'ts

Read more

🎓 Building Wealth by Investing in Education: A Strategic Guide for Professionals

Read more

📈 “Should I Sell My Company Stock?” A Mid-Year Equity Checkup for Tech Professionals

Read more

"One Big Beautiful Bill” & What It Means for High‑Earning Millennial & Gen-Z Professionals

Read more

Planning to Care for Family: Balancing Financial Goals and Personal Responsibilities

Read more

Mid-Year Money Moves: 5 Smart Tax Strategies for Equity Holders & High-Earning Professionals

Read more

Quarterly Estimated Taxes: Do You Owe by June 15? A Guide for High-Earning Professionals

Read more

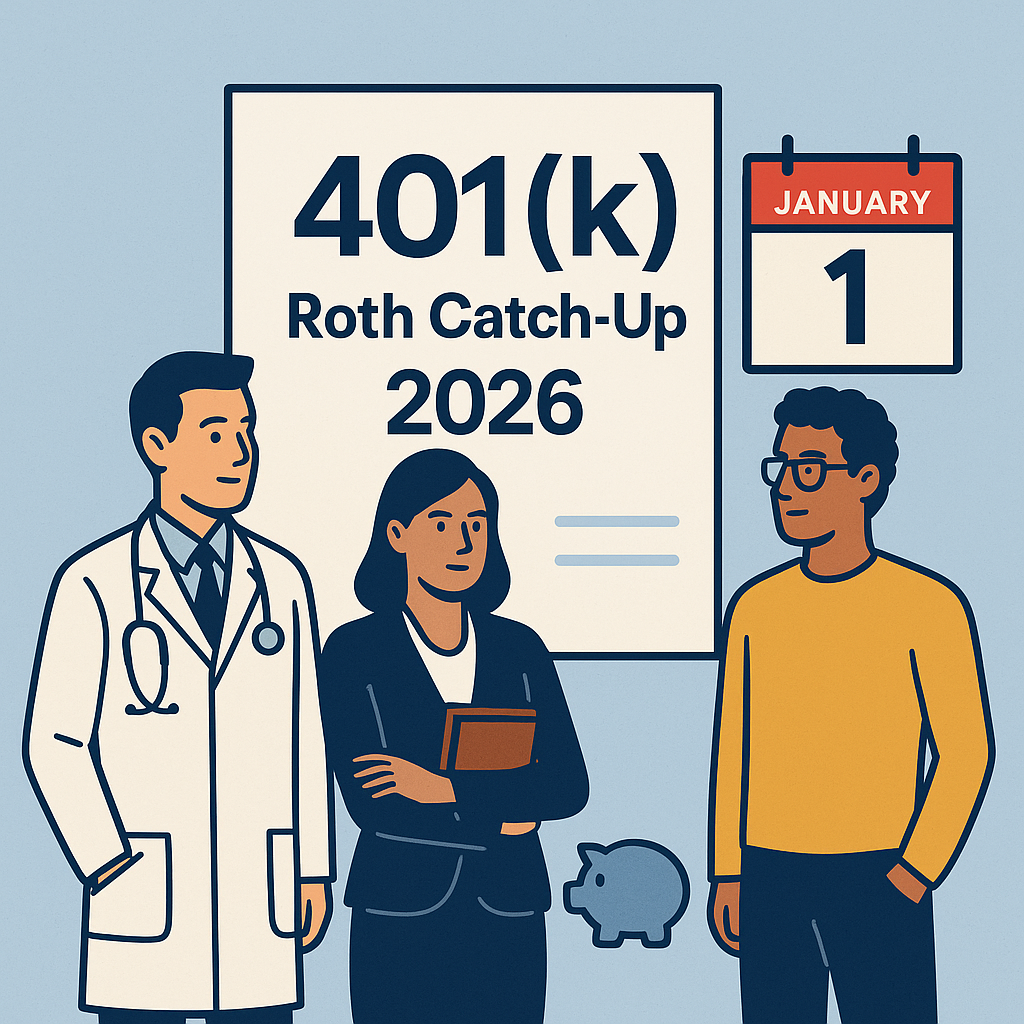

The Roth Catch-Up Mandate Is Coming: 5 Concrete Moves High-Earners Should Make in 2025

Read more

Why Your Property Tax Bill Might Spike This Year—and What You Can Do About It

Read more

May Is the Perfect Time to Review Your Tax Return—Especially If You Have Equity Compensation

Read more

Strategic Tax Planning After Filing Season

Read more

Last-Minute Tax Strategies for High-Earning Professionals

Read more

Beyond the Paycheck: A Tactical Guide to Equity Compensation for High-Performing Professionals

Read more

2025 Update: RMDs and Inherited Retirement Accounts

Read more

Social Security Fairness Act: What Retirees Need to Know

Read more

Year-End Tax Strategies You Cannot Afford to Miss

Read more

Inflation Is Eroding the Value of Your Credit-Card Rewards

Read more

A Historical Look at Interest Rates and What to Expect Before the September Fed Meeting

Read more

Investing for the Long Haul: Why Time Matters More Than Timing

Read more

Feeling the "Vibecession"?

Read more

Your Role & Responsibilities an an Agent in a Power of Attorney (POA)

Read more

Five Smart Strategies to Protect Against Inflation

Read more

View more