Market Volatility in 2026: What High Earners Should Actually Do With Their Portfolio Right Now

Market Volatility in 2026: What High Earners Should Actually Do With Their Portfolio The last two weeks have been a stress test. In late February, a Supreme Court challenge to the administration's...

Read more

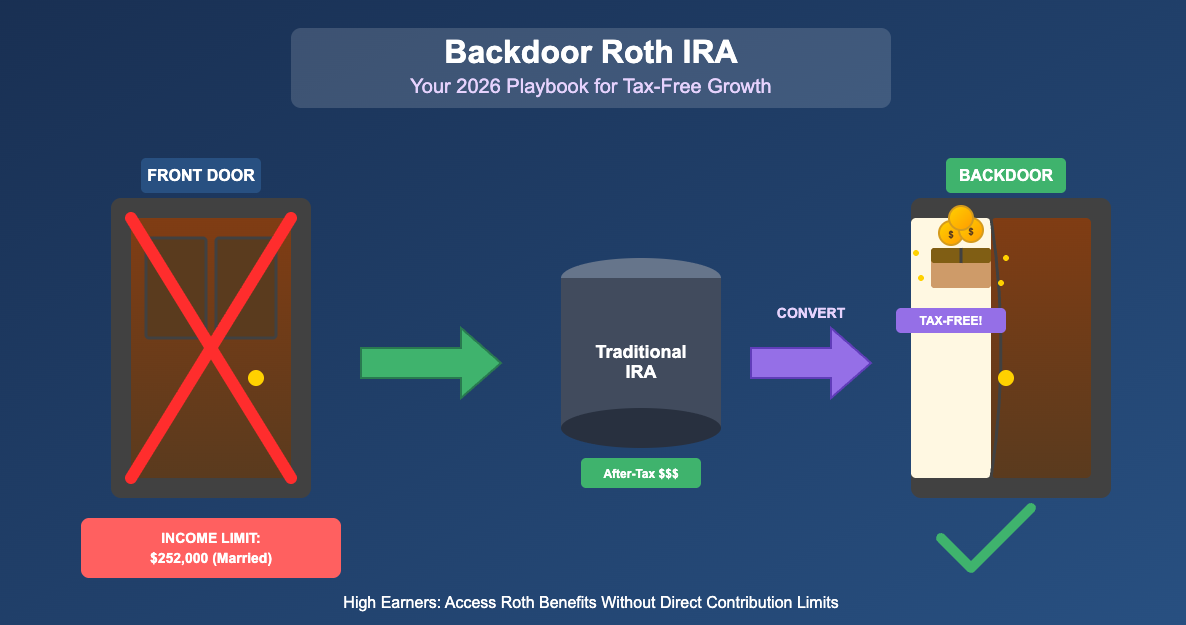

Backdoor Roth IRA Strategy for 2026: How High Earners Can Still Access Tax-Free Growth

Backdoor Roth IRA Strategy for 2026: How High Earners Can Access Tax-Free Growth If you earned over $250,000 last year, you've likely discovered a frustrating reality: the IRS won't let you...

Read more

Tax Season 2026: Why Filing Smart Beats Filing Fast

Tax Season 2026: Why Filing Smart Beats Filing Fast The IRS opened for business on January 26, and if your inbox resembles mine, you've been flooded with reminders to file early and claim your...

Read more

2026 Tax Planning for High Earners: How to Turn Updated Rules Into an Advantage

2026 Tax Planning for High Earners: How to Turn Updated Rules Into an AdvantageIntroduction: Why 2026 Tax Planning Deserves Attention Now Most people approach taxes by looking backward. Effective...

Read more

Why You Should Recalibrate your Retirement Strategy BEFORE the New Year

❄️ “2026 Is Calling”: Why You Should Recalibrate Your Retirement Strategy Before the New YearAs we approach the final week of 2025, many of the numbers that govern how much you can shelter from...

Read more

How to Maximize Year-End Tax Moves Before December 31st

How to Maximize Year-End Tax Moves Before December 31stAs the year winds down, many high-earning professionals - especially physicians finishing a busy quarter, attorneys closing cases, and tech...

Read more

When “Fixed” Isn’t the Default: Navigating ARMs for Young High-Earners

When “Fixed” Isn’t the Default: Navigating ARMs for Young High-Earners As a high-earning young professional—maybe you’re a tech founder raising your Series B, an attorney fresh off partner track, a...

Read more

Open Enrollment - Dos and Don'ts

IntroductionOctober and November mark open enrollment season at most employers. For high-earning professionals—physicians, attorneys, tech leaders, business owners—this is one of the few times each...

Read more

🎓 Building Wealth by Investing in Education: A Strategic Guide for Professionals

🎓 Building Wealth by Investing in Education: A Strategic Guide to using Education to achieve/enhance your financial success Whether you're saving for your child’s college tuition, funding your own...

Read more

📈 “Should I Sell My Company Stock?” A Mid-Year Equity Checkup for Tech Professionals

📈 “Should I Sell My Company Stock?” A Mid-Year Equity Checkup for Tech Professionals It’s July—halfway through the year, and right around the time when many public tech companies report earnings,...

Read more

"One Big Beautiful Bill” & What It Means for High‑Earning Millennial & Gen-Z Professionals

“One Big Beautiful Bill” & What It Means for High‑Earning Millennial & Gen-Z ProfessionalsAfter months of chatter and a whole lot of disagreement, One Big Beautiful Bill (OBBBA)—has landed,...

Read more

Planning to Care for Family: Balancing Financial Goals and Personal Responsibilities

Planning for Family Care: Balancing Financial Goals and Personal Responsibilities As a financial advisory firm, we often encounter high-earning young professionals who face the complex decision of...

Read more

Mid-Year Money Moves: 5 Smart Tax Strategies for Equity Holders & High-Earning Professionals

Mid-Year Money Moves: 5 Smart Tax Strategies for Equity Holders & High-Earning Professionals It’s nearly July — and while summer vacation plans may be top of mind, your tax strategy should be, too....

Read more

Quarterly Estimated Taxes: Do You Owe by June 15? A Guide for High-Earning Professionals

Quarterly Estimated Taxes: Do You Owe by June 15? A Guide for High-Earning Professionals We’re heading into June 15 — which means it’s time for many high-earning professionals to ask:“Do I owe...

Read more

The Roth Catch-Up Mandate Is Coming: 5 Concrete Moves High-Earners Should Make in 2025

If you’re 50-plus and earning more than $145,000 in FICA wages from your employer, the way you make 401(k) “catch-up” contributions is about to change—permanently. Section 603 of the SECURE 2.0 Act...

Read more

Why Your Property Tax Bill Might Spike This Year—and What You Can Do About It

🏠 Why Your Property Tax Bill Might Spike This Year—and What You Can Do About It Understanding Reappraisals, Informal Reviews, and Appeals in a Changing Property Tax LandscapeIf you’re a high...

Read more

May Is the Perfect Time to Review Your Tax Return—Especially If You Have Equity Compensation

Why Your Tax Return Tells a Bigger Story Than Just What You OweNow that Tax Day has passed, most high-earning professionals breathe a sigh of relief and move on. But if you're a tech professional...

Read more

Strategic Tax Planning After Filing Season

Strategic Tax Planning After Filing SeasonWhat to Do Now for a Better Financial Future TLDR: Now that tax filing season is over, it's the perfect time to implement strategic planning for the rest...

Read more

Last-Minute Tax Strategies for High-Earning Professionals

Last-Minute Tax Strategies for High-Earning Professionals: What You Can Still Do Before FilingTax season is in full swing, and if you're a high-earning professional—whether you're a physician,...

Read more

Beyond the Paycheck: A Tactical Guide to Equity Compensation for High-Performing Professionals

Beyond the Paycheck: A Tactical Guide to Equity Compensation for High-Performing Professionals As a physician pulling late shifts, a startup attorney negotiating term sheets, or a tech professional...

Read more

2025 Update: RMDs and Inherited Retirement Accounts

As we navigate the complexities of inherited retirement accounts, staying informed about the latest rules and regulations is more important than ever. Many non-spouse beneficiaries are familiar...

Read more

Social Security Fairness Act: What Retirees Need to Know

The signing of the Social Security Fairness Act on January 5, 2025, marks a landmark shift for many retired public servants. With outdated provisions, such as the Windfall Elimination Provision...

Read more

Year-End Tax Strategies You Cannot Afford to Miss

As the calendar year draws to a close, it's crucial to look into strategic tax planning to maximize your benefits and minimize liabilities. While some actions can be taken into the next year,...

Read more

Inflation Is Eroding the Value of Your Credit-Card Rewards

The Perks of Credit Cards and Points Using credit cards offers more than just convenience—it's a way to earn points that can be redeemed for rewards like flights, gift...

Read more

A Historical Look at Interest Rates and What to Expect Before the September Fed Meeting

As the Federal Reserve prepares for its September meeting, much attention is focused on the possibility of an interest rate cut. Economic data has been signaling the potential for policy changes,...

Read more

Investing for the Long Haul: Why Time Matters More Than Timing

Given the volatility of the U.S. stock market, I wanted to revisit an age-old investing principle that seems to have been overshadowed by the latest news and advice....

Read more

Feeling the "Vibecession"?

How do you feel about the state of the economy? In more contemporary terms, what are your "vibes" telling you? Are you feeling confident...

Read more

Your Role & Responsibilities an an Agent in a Power of Attorney (POA)

A Helpful Guide on the Different Types of Powers of Attorney A power of attorney (POA) can grant you certain authority and specific responsibilities. While the extent...

Read more

Five Smart Strategies to Protect Against Inflation

Do you remember the year when a gallon of gas cost just $0.63? Depending on your age, you might not! That year was 1978. When the prices of goods and services rise in...

Read more

Unearth Your Hidden Goals: Why Talking to a Financial Professional Helps

Goal-setting. It's the bread and butter of success across so many domains. But are you only scratching the surface? Dive deeper. A financial professional doesn't...

Read more

How to Stop Subconsciously Sabotaging Your Financial Goals

How often do you set new financial goals? How often do you achieve them? Most of us aren’t very successful with our goals, even when we have the best intentions and...

Read more

IRS Changes Inheritance Rules: Protecting Your Legacy

The IRS recently updated some rules about trusts that could make your heirs accidentally liable for capital gains taxes.1 It's another quiet change that could severely...

Read more

Top 4 Social Media Money Scams & How to Spot Them

Believe it or not social media scams have been picking more pockets than any other scam today--including phone call and text fraud.1 There have been more than $2.7...

Read more